Loan Settlement – Advantages & Disadvantages

By Karaz Se Mukti Team

People often confuse “loan settlement” with “loan closure.” The two words sound similar but lead to sharply opposite outcomes. A closed loan signals that you repaid every rupee you promised; a settled loan signals that you did not—and banks never forget this distinction. Understanding exactly what you stand to gain, and what you stand to lose, is the only way to make the right call.

📊 Snapshot: Benefits vs. Risks of Loan Settlement

| ✅ Advantages | ❌ Disadvantages |

|---|---|

| Offers immediate relief from overwhelming debt and collection pressure | Severely damages CIBIL score, dropping it by 75–100 points (or more) |

| Lowers total repayment amount—pays only a part of what’s owed | “Settled” status remains on credit report for up to 7 years |

| Helps avoid legal action, harassment, or bankruptcy proceedings | Makes future loan/credit card approvals extremely difficult, and for secured loans like mortgages, near-impossible |

| Brings faster resolution with a one-time lump-sum payment | May face higher interest rates if any credit is extended in the future |

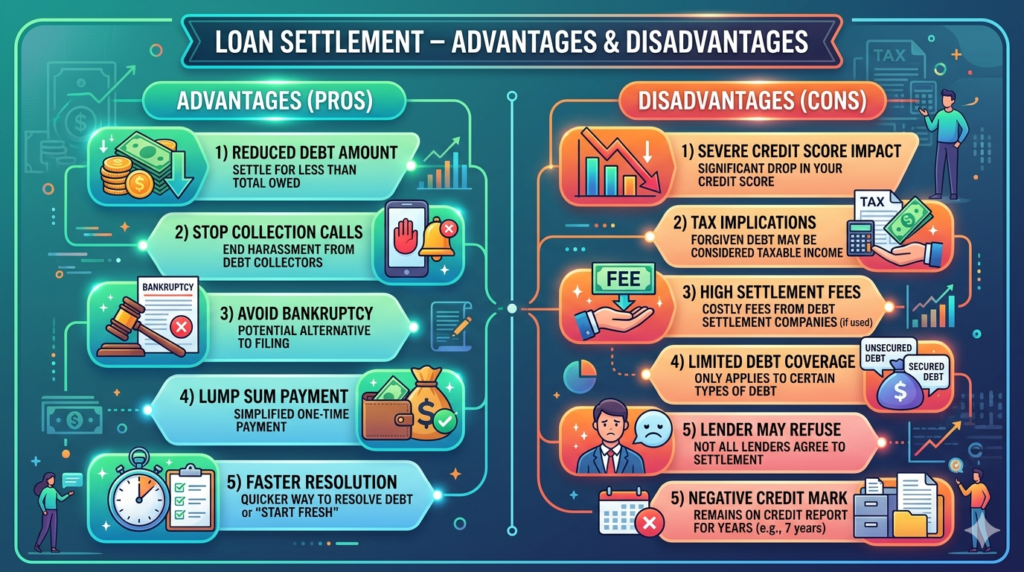

✅ The Seductive Sugar-Coating: The Alluring Benefits of Loan Settlement

It would be naive to dismiss the benefits—in a genuine crisis, they are the only bridge back to solid ground.

1. An Immediate Lifeline of Financial Relief

The biggest and most obvious advantage is that settlement ends the immediate siege. The moment a settlement is reached and the lump sum is paid, all follow-ups from recovery agents and legal proceedings from the bank stop—bringing immense peace of mind to someone who has been under severe financial and emotional stress for months.

2. A Drastic Reduction in Overall Debt

Through settlement, you are not just stopping the harassment; you are legally extinguishing a large portion of your debt. Instead of repaying a crushing ₹5 lakh loan, you might settle the entire account for a single payment of ₹3 lakh, with the bank writing off the remaining ₹2 lakh. This significantly reduced burden can be the difference between perpetual insolvency and a manageable financial reset.

3. A Shield Against Legal Action and Bankruptcy

A prolonged loan default often leads to severe legal consequences, and in the worst-case scenario, bankruptcy. The legal and social stigma of insolvency can be a life-long shadow. Loan settlement acts as a crucial shield against this—it’s a negotiated agreement with the lender to close the matter permanently, preventing it from escalating into a court battle or a formal declaration of bankruptcy.

🚫 The Bitter Aftertaste: The Deep, Lasting Damage of Loan Settlement

The benefits, immediate as they are, come at an immense hidden price. The “settled” stamp on your credit report acts exactly like a permanent red flag visible to every financial institution for years—it broadcasts, “I couldn’t fully repay my debt,” even if your circumstances were genuinely tragic.

1. The Wrecking Ball: Your CIBIL Score Plummets

If a missed payment is like a crack in a window, a loan settlement is like a wrecking ball. It is viewed as one of the most severe negative credit behaviors. You can expect your CIBIL score to take a catastrophic hit, typically dropping by 75 to 100 points or more. In many cases, this can instantly push a decent score into the “subprime” category, fundamentally altering your financial identity.

2. An Inescapable Financial Scar for 7 Long Years 📅

You can rebuild your income in a year or two, but a settled status remains on your credit report for up to seven years. This means any financial institution—for nearly a decade—will see that a past loan was not honoured in full and almost certainly reject any fresh loan or credit card application.

3. A Blockade to All Future Borrowing—Especially for Big Goals

This is where the real-world pain is felt most acutely. The “settled” status acts as a near-permanent blockade:

- Unsecured Loans (Personal/Credit Cards): Approval becomes extremely difficult in the medium term, and even if granted after years, the interest rate will be punitive to compensate for the high risk.

- Secured Loans (Home/Car): This is the hardest hit. For a mortgage, the single most important loan most people will ever take, a past settlement on the credit report is often an outright rejection trigger—putting the dream of home ownership on ice for the better part of a decade.

4. It’s a “Solution” That Consumes Future Opportunities

Settlement is not a cheat code; it’s a trade-off. You trade your present distress for a discount, but you pay for it with a 7-year dent in your creditworthiness. It solves an immediate cash-flow problem by largely destroying your ability to access credit for a significant portion of your working life. The initial relief can quickly turn into regret when you fail to get a crucial education loan or a business loan to capitalise on a golden opportunity.

🤔 Settlement vs. Alternatives: Choosing Your Hard

| Factor | Loan Settlement | Debt Consolidation |

|---|---|---|

| Best For | Zero repayment ability (job loss, permanent disability). | High-interest debt with stable income. |

| CIBIL Score | Drops 75–100+ points; “Settled” mark for 7 years | No direct negative mark; can improve score over time. |

| Future Loans | Severely restricted for years. | Remains accessible with good repayment. |

| Financial Health | Provides immediate relief but leaves a lasting scar. | Reorganises debt, potentially lowers EMIs, and protects credit health. |

🚑 When Settlement is Genuinely the Right (and Only) Call

- Permanent Income Cessation: A severe, permanent disability preventing any future work.

- Complete Asset Exhaustion: A medical catastrophe that has fully wiped out all savings, insurance, and family assets.

- The Bankruptcy Alternative: When the lender has initiated legal proceedings, and settlement is the only way to avoid a formal, long-term insolvency process.

In these extreme, “zero-option” scenarios, settlement isn’t a choice; it’s a necessary surrender.

Final Takeaway: A Quick Decision-Making Checklist

Consult this flowchart to guide your decision. It’s designed to help you quickly determine the most suitable path based on your current financial reality.

┌─────────────────────────────┐

│ Struggling with debt repayments │

└─────────────┬───────────────┘

▼

Is your financial hardship temporary?

├── YES ──► Do you have a good credit score?

│ ├── YES ──► Speak to lender about restructuring/moratorium

│ └── NO ──► Explore debt consolidation to reduce interest burden

│

└── NO ──► Is your income loss permanent and severe (disability, etc.)?

├── YES ──► Exhausted all savings/assets?

│ ├── YES ──► Loan settlement may be last resort

│ └── NO ──► Liquidate assets to close loan fully

└── NO ──► Restructure loan or explore debt consolidation

✍️ Author: KARAZ SE MUKTI TEAM

📞 +91 75080 25178 — ya mail bhejo: info@karzsemukti.in, karzsemukti1@gmail.com

Follow us on: